Summary

Payroll services in India has many important components like PF, gratuity, HRA, LTA, etc. You as a foreign business, need to follow these religiously to attract and retain top talent in India. Many payroll outsourcing services in India will help you do that through their integrated systems.

Payroll services in India are a huge boon to foreign businesses hiring talent in India. Why? Because they’re smarter, faster, and far more local than you’d expect. For global businesses, payroll services in India are now key to keeping things legal and trouble-free.

The right payroll outsourcing services in India can take the entire payroll load off your plate while you’re expanding your team in the country. Also, today’s payroll outsourcing services in India don’t just manage the payroll process for you; they adapt to local laws, catch exceptions, and keep your data secure.

In this blog, we’ll cover:

-

- How does payroll actually work in India?

- What’s changed in recent years?

- Must-have features in a payroll partner

- The exact steps to process payroll correctly

- Why compliance here isn’t copy-paste?

- How Remunance helps global teams stay on track?

Let’s start with it.

Why Payroll Services in India Are Necessary?

Managing payroll in India is a relatively challenging task when you’re unaware of its ever-changing labor laws. For foreign businesses, the challenge lies in aligning centralized global systems with India’s fragmented compliance setup. That’s where payroll services in India come into play.

What’s often not talked about is the role of micro-compliance mapping. India isn’t one country in payroll terms; it’s 28 states with different rules. Each Indian state has its own tax rules, leave policies, and statutory thresholds. The best payroll services in India now use geo-tagged HRMS tools to adapt to regional laws in real time. It’s beyond automation, it’s intelligent localization.

What sets modern payroll outsourcing services in India apart is how they handle exceptions. Be it mid-cycle bonus adjustments or tax regime switches, smart systems catch what legacy CRMs often miss.

Data security is no longer optional. With India’s new DPDP Act kicking in, payroll service providers in India are prioritizing local data hosting, consent-based access, and AI-led fraud detection.

Payroll isn’t complex because of people; it’s complex because of rules, and India has plenty. The right payroll outsourcing services in India know how to simplify the chaos while keeping every line item audit-ready.

So what I’m really trying to say here is, look for online payroll services in India that offer not just tech integrations but rule-based precision. Because compliance here isn’t a one rulebook thing, it’s case-by-case.

Evolution of Payroll Services in India

Stepping into India’s booming market for business expansion is an obvious smart decision. However, your payroll process needs to be sharp for this expansion. And today’s payroll in India looks nothing like it did five years ago. Consequently, the payroll services in India have also evolved over the years. Now, payroll services in India take care of elements that are tied to culture, compliance, and credibility. Let’s get into the details of that.

Make Local Rules Work in Your Favor

India’s tax laws and labor codes vary not just by sector, but by state. Good news? The best payroll services in India handle all that complexity for you. No more getting lost in deductions or fumbling with region-specific holidays. Localization is built in.

Read: Payroll and Compliance Management in India

Use the Tools You Are Already Familiar With

Modern payroll service providers in India aren’t working in silos. They’re syncing with your global HCM systems, ERPs, and finance tools. Whether you’re using SAP, Workday, or something leaner, your payroll won’t be left behind.

Strong Security System

With rising concerns over data leaks, providers are stepping up. Some are even experimenting with blockchain for tamper-proof salary logs. And encryption? It’s not an add-on anymore, it’s the standard.

Give Employees What They Actually Want

No one wants to chase down an HR manager for a payslip. That’s why smart companies use online payroll services in India with full employee self-service (ESS) portals. Employees can track leaves, view tax splits, and update details, all from their phone. It’s simple, it’s fast, and yes, it matters.

Ready for Freelancers and Flexible Teams

Full-time staff aren’t your only concern anymore. India’s gig economy is exploding, and payroll systems are keeping up. Payroll outsourcing services in India now handle hourly, project-based, and milestone-linked pay with zero friction. Need UPI payouts or wallet integration? That’s part of the package.

Speed up Your Expansion Compliantly

Whether you’re hiring 5 or 500, compliance needs to be solid. From PF filings to bonus calculations, payroll outsourcing services in India manage the messy backend so your India rollout doesn’t hit any roadblocks.

Let’s end this section by recalling the phrase: “Pay delays lose trust faster than bad Wi-Fi.”

Read: Top payroll outsourcing companies in India

Want to learn about payroll services in India in more detail?

We’ve got your back!

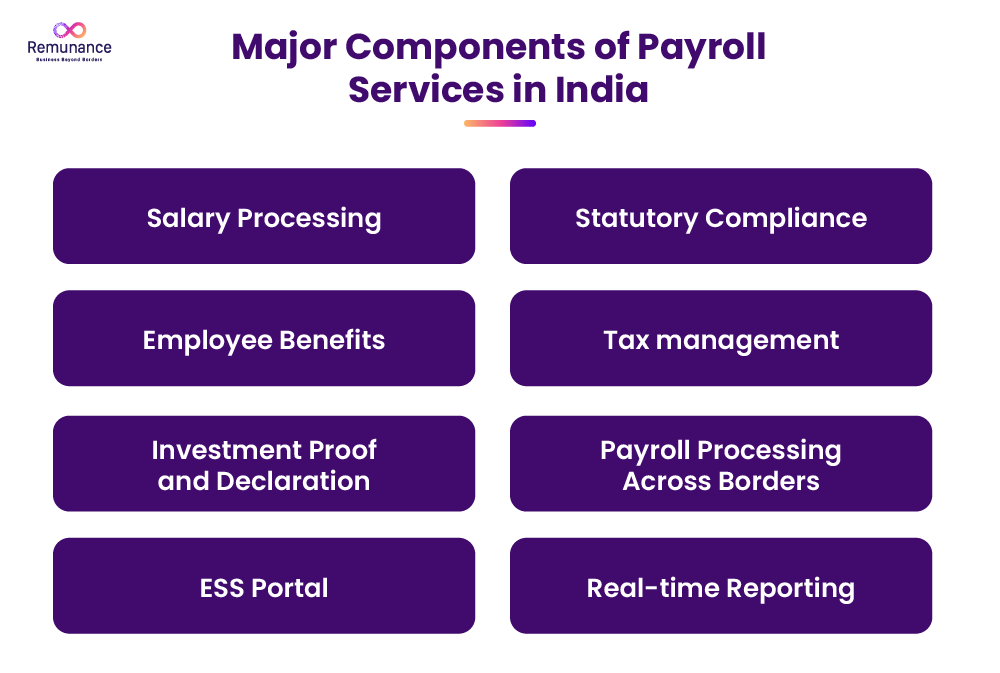

Key Components of Payroll Services in India

Key elements of payroll services for Indian businesses.

Modern payroll services in India are built to do much more than process salaries. They manage everything from maintaining documentation to employee experience without skipping any important part.

Salary Structuring & CTC Management

Payroll systems handle fixed, variable, and flexible components. This includes HRA, LTA, bonuses, and reimbursements.

Statutory Compliance Automation

From EPF, ESI, and TDS to state-specific professional taxes, auto-updates keep things fully compliant. This is a must-have in every payroll outsourcing service in India.

Attendance, Leave & Shift Integration

Seamless syncing with HRMS and biometric tools ensures accurate work-hour tracking. There’s no room for any mismatches and no need for any manual inputs.

Tax Regime Optimizers

New-age platforms help employees choose between the old and new tax regimes with real-time calculators.

Investment Proof & Declaration Module

AI-based scanning validates proofs instantly. It reduces fraud and speeds up payroll cycles.

Multi-Location Payroll Processing

Essential for businesses across states. Each region’s compliance is managed without a separate setup.

Accounting & ERP Integration

Payroll syncs with tools like SAP, Zoho, and Tally for ledger updates and journal entries, live and accurate.

Employee Self-Service Access

Staff can download payslips, update bank details, or declare taxes; no HR follow-ups needed.

Global Payroll Consolidation

For MNCs, global payroll services in India centralize operations, ensuring compliance across multiple countries.

Real-Time Reporting & Dashboards

From CTC analytics to compliance alerts, everything is visual, exportable, and audit-ready.

By adopting third-party payroll services in India, companies cut risk and scale faster. Whether it’s a startup or an enterprise, payroll outsourcing services in India help reduce workload and ensure accuracy.

No wonder global payroll services in India are becoming the preferred route for multinationals expanding in Asia.

Step-by-Step Process of Payroll Services in India

Now, let’s see what the mandatory steps are to follow to process payroll in India. Here’s the correct order for it:

1. Get Your Employee Data in Place

Collect Aadhaar, PAN, UAN, bank details, and full salary structure before anything else. Most payroll providers in India now sync this automatically with your HR or onboarding tool.

2. Set up Attendance and Leave Data

Whether it’s biometric, app-based, or GPS tracking, attendance feeds straight into payroll. Good payroll outsourcing services in India adjust salaries based on real-time work logs.

3. Build a Flexible Salary Structure

Beyond basic + HRA, companies are now adding fuel cards, bonuses, and meal allowances. It’s not just about attracting talent; it also makes tax planning smoother for both sides.

4. Run the Salary Calculations

Here’s where gross meets net. Deductions, bonuses, and unpaid leaves, all of it is processed. Before you hit “transfer”, most teams do a quick approval check from finance or HR.

Read: Comprehensive Salary Calculations in India and Payroll Optimization

5. Disburse Salaries and Send Payslips

Payouts go through bulk bank transfers; payslips are auto-emailed to employees. Top payroll services in India offer encrypted, API-based integrations with banks for this step.

6. Handle the Monthly Government Filings

This includes PF (ECR), ESI, and TDS filings, plus generating Form 16 at year-end. Most payroll outsourcing services in India now do this without much manual effort.

7. Reconcile Payroll and Lock in Reports

This is the audit trail; cross-check payout files with what actually got credited. The best systems keep logs of who approved what, and when.

8. Push Data to Government Portals via APIs

Modern payroll systems skip manual uploads. Returns, challans, and tax files go directly. This keeps your payroll compliance in India solid and error-free.

Added Benefits of Payroll Services in India

As I said, when people hear “payroll,” they usually think of payslips and tax deductions. But it’s so much more than that. It requires local know-how and a brain to keep up with your competitors and retain the best talent. That’s why payroll services in India are always in demand. Let’s look at the benefits businesses get from them.

What Foreign Companies Really Gain?

Here’s what doesn’t always show up in the brochures, but matters big time:

Cross-border compatibility

-

- Most payroll providers in India can sync with your global HR or ERP systems. That means less manual work and smoother data syncing.

- They also help translate Indian payroll data into formats your finance team can actually use.

Faster onboarding and happier hires

-

- Local payroll outsourcing services in India often handle bank account setup, benefits enrollment, and documentation.

- Your employees get paid on time from day one, even if you’re managing things from another time zone.

Now let’s talk about a relatively uncommon but crucial one: data hosting.

India has specific data localization laws. If your employee payroll data is hosted outside India, that could be a compliance risk.

Reputable payroll outsourcing services in India host data locally and securely; problem solved.

Mandatory Checklist for Payroll Services in India

If you’re handling payroll services in India, there are a few components you just cannot go without. Here are some often-overlooked yet mandatory essentials that every payroll team needs to stay sharp on:

Digital Payment Enforcement

Gone are the days of paying wages in cash. Today, it’s compulsory to process salaries through digital channels, especially if you’re using online payroll services in India. This ensures legal traceability and keeps you aligned with RBI norms.

Region-specific Professional Tax

While offering payroll outsourcing services in India, you need to account for state-specific Professional Tax rules. Some states change their slabs annually, so local compliance checks are a must.

Wage Code Readiness

While the new labour codes are pending implementation, prepping your payroll systems to accommodate changes in wage definitions, overtime, and gratuity is considered a good compliance practice and might soon be non-negotiable.

CTC Structure Disclosure

Today’s labour inspections pay close attention to how clearly your offer letters reflect earnings, allowances, and deductions. Vague or bundled salary structures? Not worth the risk.

Gender & Workforce Data Reporting

For companies with 10+ employees, you’re expected to maintain updated gender-wise data for compliance reports and POSH audits. Global payroll services in India also need to ensure this for international entities operating locally.

Monthly Reconciliation Rituals

Whether you’re using in-house tools or the best payroll services in India, monthly cross-checks between payroll outputs, bank transactions, and compliance filings (like EPF, ESI, and TDS) are non-negotiable. One mistake can trigger a chain of penalties.

Curious how to effectively manage payroll services in India?

EOR should be your obvious choice

How Remunance Helps Foreign Businesses with Payroll Services in India?

Now that we’ve talked about the dos and don’ts of payroll services in India, let’s see how Remunance fits into your checklist. Rather, how Remunance can really contribute to your India expansion.

To start with, Remunance has over two decades of experience in making payroll effortless for global companies. We don’t just process payroll for the namesake. Remunance becomes your on-ground payroll partner, managing tax deductions, helping you with statutory rules, and even handling multi-currency payouts.

With teams across 7 Indian cities and a workforce of 1,123 (and counting), we’re always close to the action, ready to ensure your payroll runs smoothly and is fully compliant with India’s evolving 2025 regulations.

Need tech-enabled simplicity? Our online payroll services in India give you secure, 24/7 access to everything. But remember, we are NOT a software. We have our dedicated team of experts to take care of and support you with everything.

And if you’re still in the experiment phase with India? You don’t need to set up a full legal entity. As an Employer of Record, Remunance helps you build and manage your team while we take care of compliance, HR, and payroll services in India.

Why foreign companies choose Remunance for their payroll outsourcing services in India:

-

- ISO-certified systems for secure payroll outsourcing services in India

- Presence in 22+ countries, offering truly global payroll services in India

- Named a Thought Leader in the EOR and payroll domain

- Trusted by clients as one of the best payroll services in India

- Bagged the title of GPTW multiple times

At Remunance, we keep things transparent, fast, and worry-free, so you can focus on the team and building a connection with them.

About Remunance

Remunance is an Employer of Record (EOR) services provider in India, helping global companies hire, manage, and support full-time employees without setting up a local entity. We take care of HR, payroll, compliance, and benefits so businesses can focus on growth while building their teams in India with confidence.

Remunance enables businesses from UK, Australia, Canada, France, US, and the Middle East to recruit, hire, and manage workforce and benefits in India.

FAQs

What’s the difference between CTC, gross salary, and net salary?

CTC is the total cost of hiring someone; salary, PF, gratuity, insurance, the works. Gross salary is the employee’s earnings before deductions. Net salary is the final amount the employee takes home. CTC helps us budget; net salary is what they actually feel in their wallets.

Why is EPF deducted from my salary, and where does it go?

Employers deduct EPF from employee’s salaries as part of their retirement savings; it’s not a loss, it’s a long-term gain. Employers match the employee’s contribution too, and both go into your EPF account. It’s a government-backed safety net to ensure the employees have got financial security when you decide to stop working someday.

What documents do employees get during salary payment?

Every month, employers share a payslip with the employees; it’s like a mini report card of their salary. It breaks down what they’ve earned, what’s been deducted (like taxes, EPF), and what hits their bank account. At year-end, employers also give Form 16 to help them file their taxes easily.

Is professional tax applicable to everyone in India?

As an employer, the companies deduct professional tax from salaries only if it applies, based on state rules and income slabs. It’s not the same across India. Some employees, like senior citizens or those with disabilities, are exempt. So no, professional tax doesn’t apply to everyone; it depends on the situation.

What is Form 16, and who needs it?

The Form 16 is a tax summary we hand over to our employees. It shows how much employers paid them and how much tax they deducted. If they’ve cut TDS from the employee’s salary, they’re required to give it, usually by mid-June so that the employees can easily file their income tax returns.

Recent

Also read

How Does the Payroll Calendar in India Work?

https://remunance.com/blog/payroll-compliance-in-india/

How to Use an Employer of Record to Manage Payroll Services?

https://remunance.com/blog/payrolling-vs-employer-of-record/

Disclaimer

This blog is created for informational purposes. Everybody is requested to seek advice from an expert before making a decision based on the information given in the blog. Remunance disclaims any liability/loss or damage caused by using the information, directly/indirectly, given in this blog.